Don't Wait, Enroll Today

IMPORTANT: If you do not elect your benefits during the annual Open Enrollment period or within 31 days of your date of hire, you will not have Roper St. Francis Healthcare health plan coverage until the next year unless you have a qualified life event as defined by the IRS.

HAVE A QUESTION?

Have a Question? Call the HR Service Center at 888-691-5729 or go to https://bsmhealth.service-now.com/hrportal

Alliance Save

With the Alliance Save plan, you still have the same comprehensive protection and provider network as our Alliance Prime and Alliance Flex plans. You also gain greater flexibility and control over your medical expenses.

The Alliance Save plan is a high-deductible health plan option that also enable you to save toward your healthcare expenses in a tax-advantaged Health Savings Account (HSA). Roper St. Francis Healthcare will contribute up to $1,100 into your HSA.

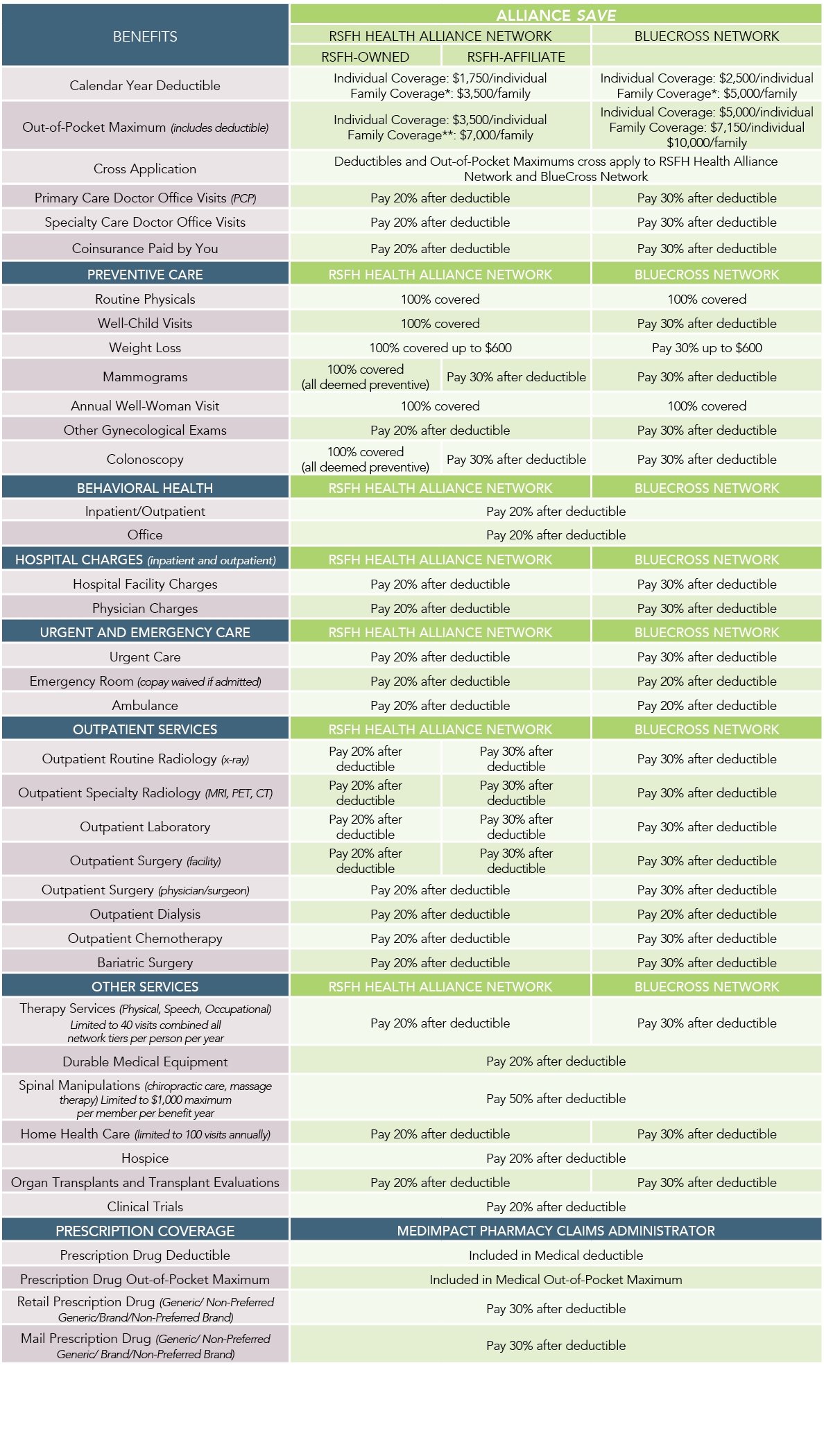

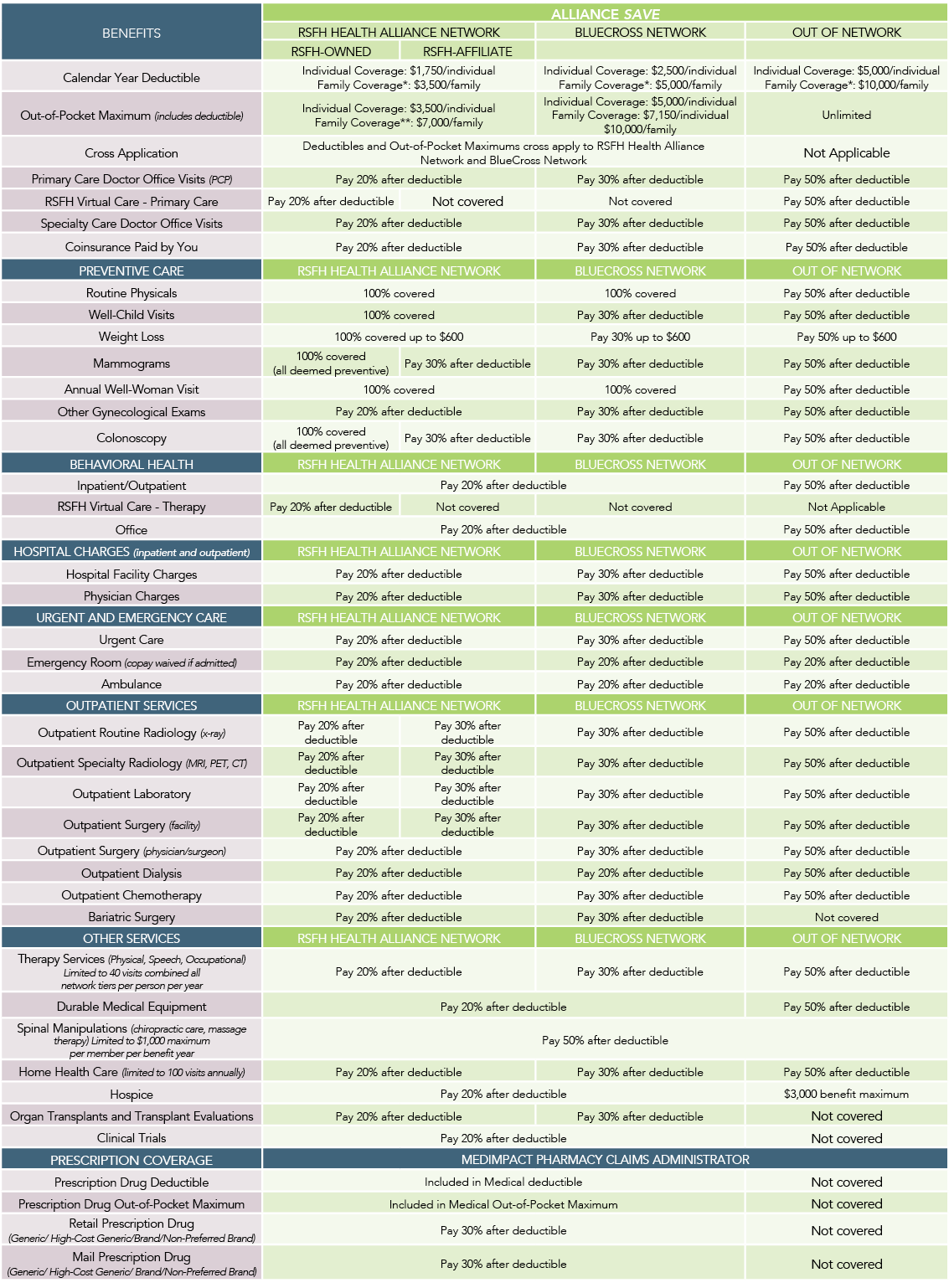

Coverage for Frequently Used Services - Alliance Save

2024 Coverage

(Click on the chart below to increase its size.) 2023 Coverage

2023 Coverage

(Click on the chart below to increase its size.)

Contribution Rates - Alliance Save

* Teammates with a hire date, status change, or life event with an effective date from January 1, 2024, through December 31, 2024, will default to the Qualified status for enrollment in the 2024 and 2025 medical plans.

* Teammates with a hire date, status change, or life event with an effective date from January 1, 2023, through December 31, 2023, will default to the Qualified status for enrollment in the 2023 and 2024 medical plans

How much will Roper St. Francis Healthcare contribute to my HSA?

Alliance Save Overview

- High deductible health plan with a Health Savings Account (HSA)

- Can use RSF Health Alliance network, BlueCross Blue Shield nationwide network, or Out-of-Network providers. (Find a Provider)

- You pay 20% co-insurance after deductible (when using the RSF Health Alliance network)

- You can offset your eligible medical expenses by using funds from your tax-advantaged HSA

- Roper St. Francis Health contributes up to $1,100 into your HSA.

- Out-of-pocket maximum of $3,500 individual/$7,000 all other tiers

Alliance Save Overview

- Can use RSF Health Alliance, BlueCross, or Out-of-Network providers. (Find a Provider.)

- You pay 20% co-insurance after deductible (when using the RSF Health Alliance network)

- You can offset your eligible medical expenses by using funds from your tax-advantaged HSA.

- Roper St. Francis Healthcare contributes up to $1,100 into your HSA.

- Out-of-pocket maximum of $3,500 individual/$7,000 all other tiers